Our 2025 Global Biopharmaceuticals Leaders Study, conducted in June and July, included nearly 400 participants—comprising 323 C-level executives and 74 prominent investors—spanning large-cap, mid-cap, small-cap, micro-cap, and private biopharma companies globally.

Central Findings:

1. Bifurcated Views on Equity Market Valuations with Pessimism on Innovation, Financing, Biotech Bankruptcies, and Risk

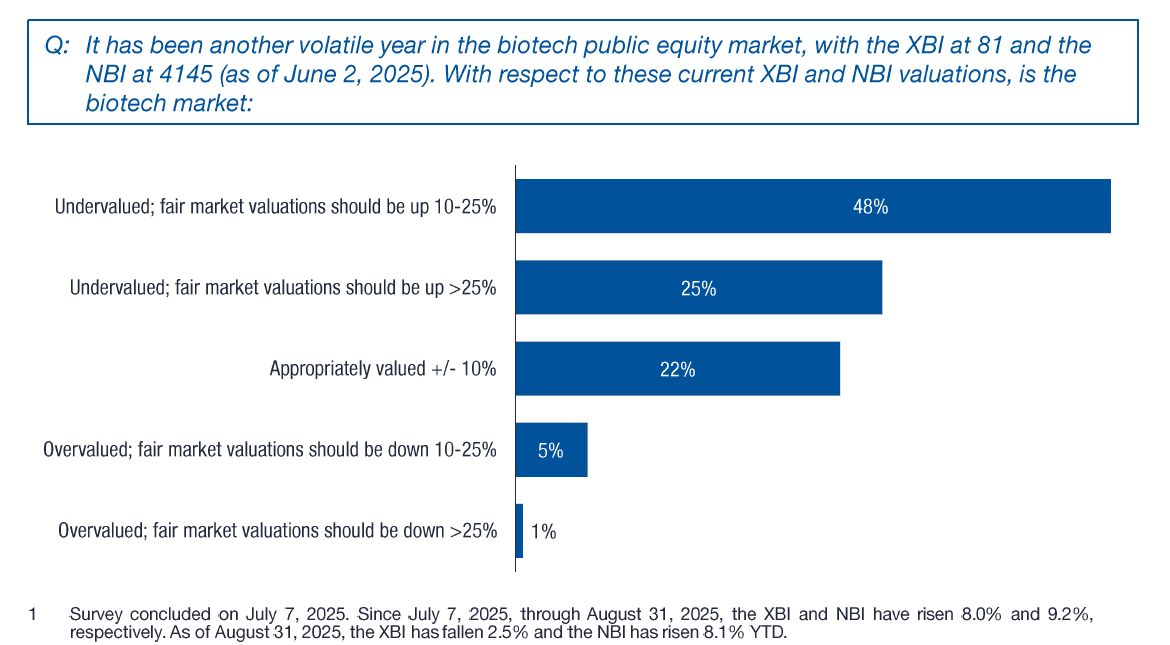

Macroeconomic uncertainties and U.S. healthcare policy continue to weigh on biotech market valuations. While large-cap and mid-cap public biopharma industry leaders see current valuations as fair or slightly overvalued, executives at small-cap, micro-cap, and private biotech companies believe their valuations remain undervalued. Concerns over an excessive number of public companies and declining financing contribute to negative sentiment, with expectations of increased biotech bankruptcies from an already elevated level.

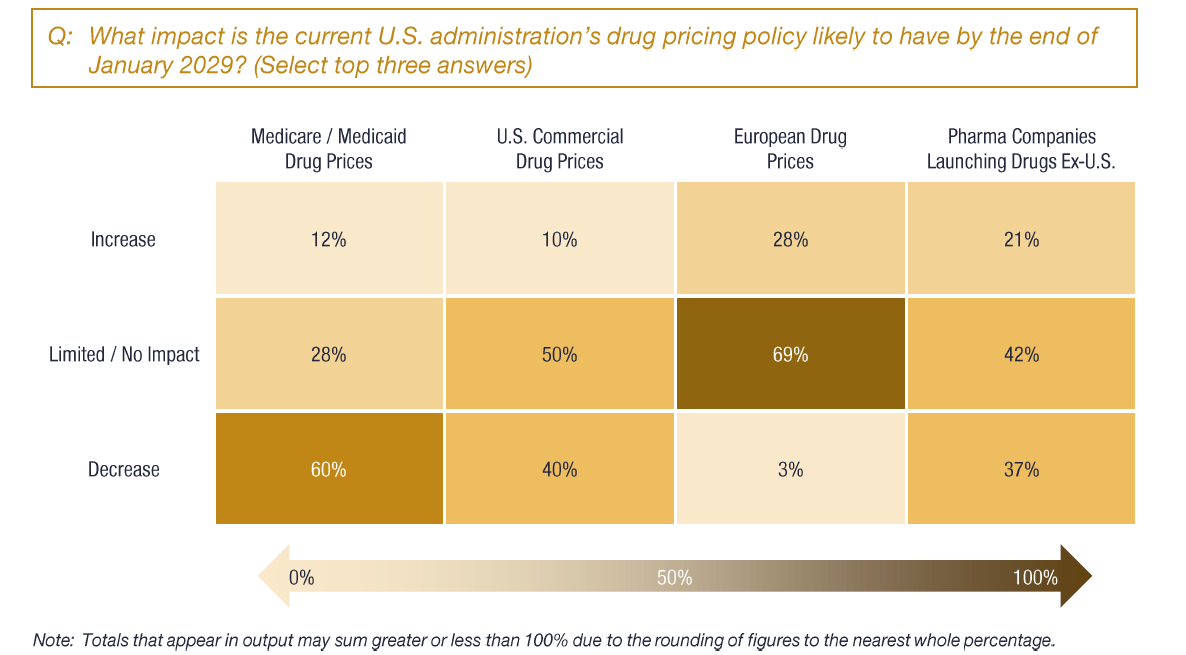

2. U.S. Administration’s Drug Pricing Policy Expected to Decrease Medicare/Medicaid and Commercial Drug Prices, Have Limited or No Impact on European Drug Prices, and Result in Fewer Biopharmaceutical Companies Launching Drugs Outside the U.S.

Drug pricing policy changes in the U.S. are expected to reduce prices under Medicare/Medicaid and in commercial markets but will likely have minimal impact on prices in international markets. Leaders believe reduced international launches and constrained commercialization could follow as a result of policy-driven headwinds.

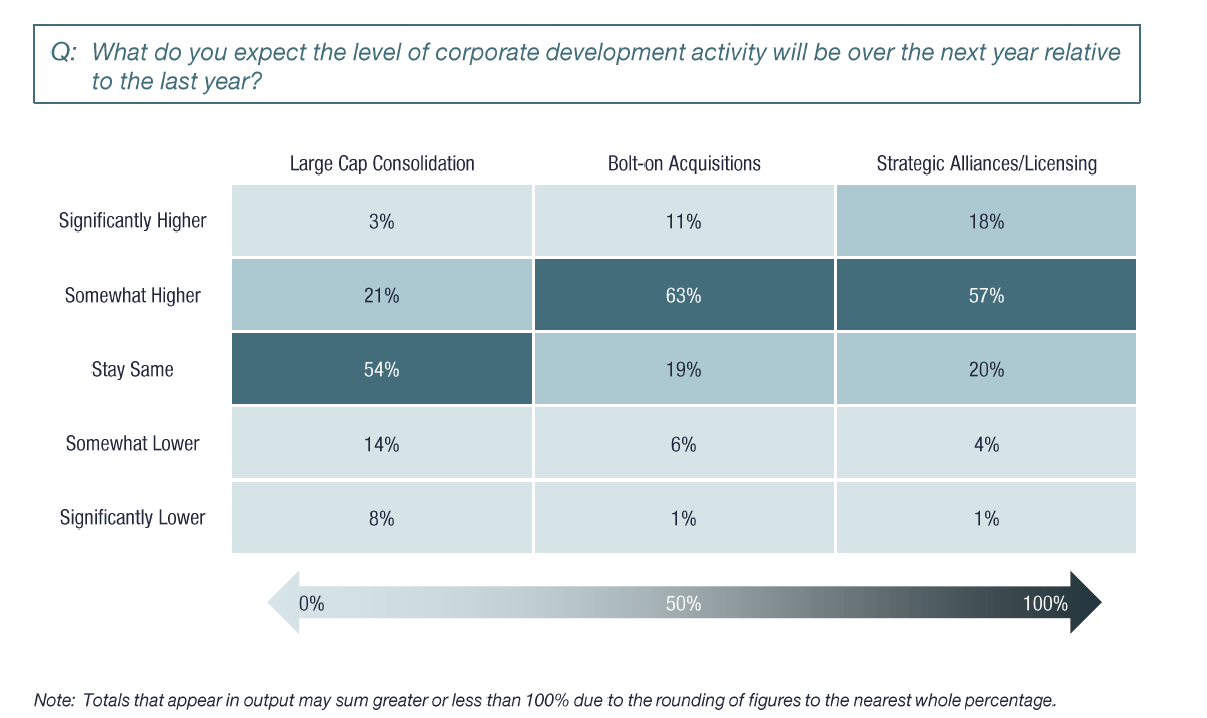

3. Large-Cap M&A, Bolt-On Acquisitions and Strategic Alliances Expected to Increase

Strategic activity in the biopharma industry is shifting. Increased expectations for large-cap consolidation are being driven by both intensifying and new pressures. Bolt-on acquisitions are expected to rise as companies seek replenishment of revenues exposed to loss of exclusivity and pricing pressure as well as growth. Strategic collaborations are increasingly viewed as an important mechanism for growth amid continued uncertainty.

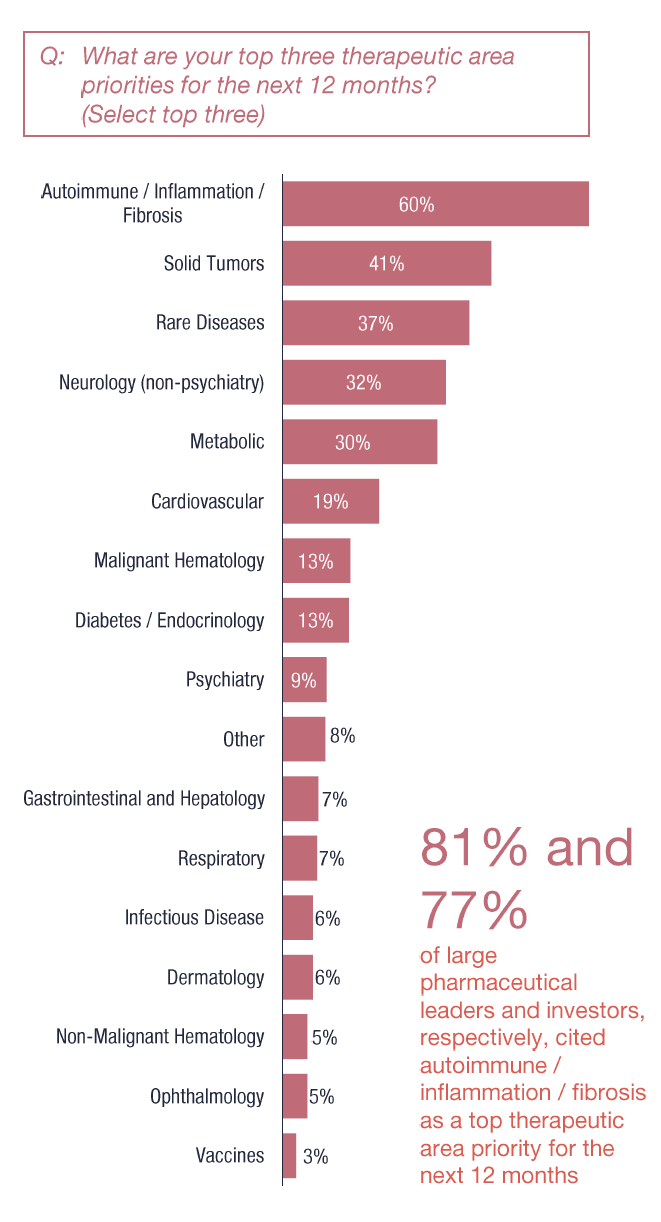

4. Autoimmune, Inflammation, and Fibrosis and Oncology Remain the Top Therapeutic Areas

Therapies focused on autoimmune, inflammation, and fibrosis remain the priority for investment and development among biopharma leaders, followed closely by oncology. Other areas such as rare diseases, neurology, and metabolic diseases remain key targets with strong growth potential, especially for smaller firms.

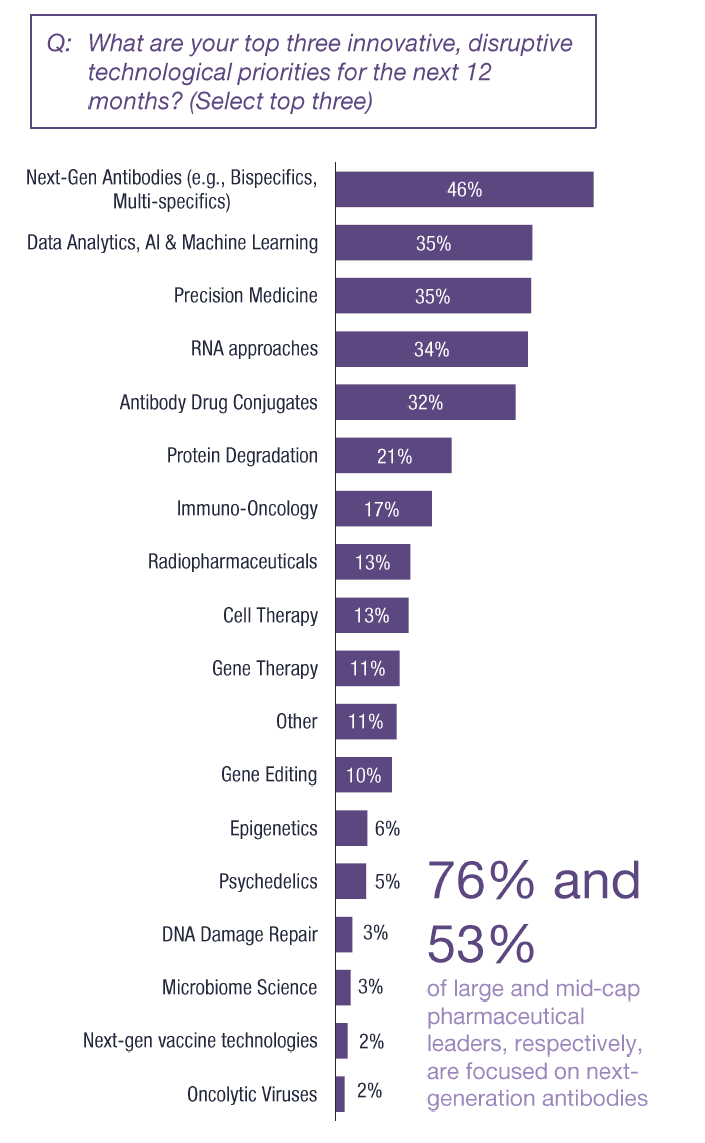

5. Next-Gen Antibodies Remains Top Technological Modality with Rising Focus on Data Analytics, Artificial Intelligence (AI) and Machine Learning (ML)

Emerging technologies like next-generation antibodies—spanning bispecific and multi-specific innovations—showcase the breadth of innovation in the sector. Data analytics, AI, and ML are increasingly being prioritized, while focus on precision medicine, RNA approaches and antibody drug conjugates remains high.

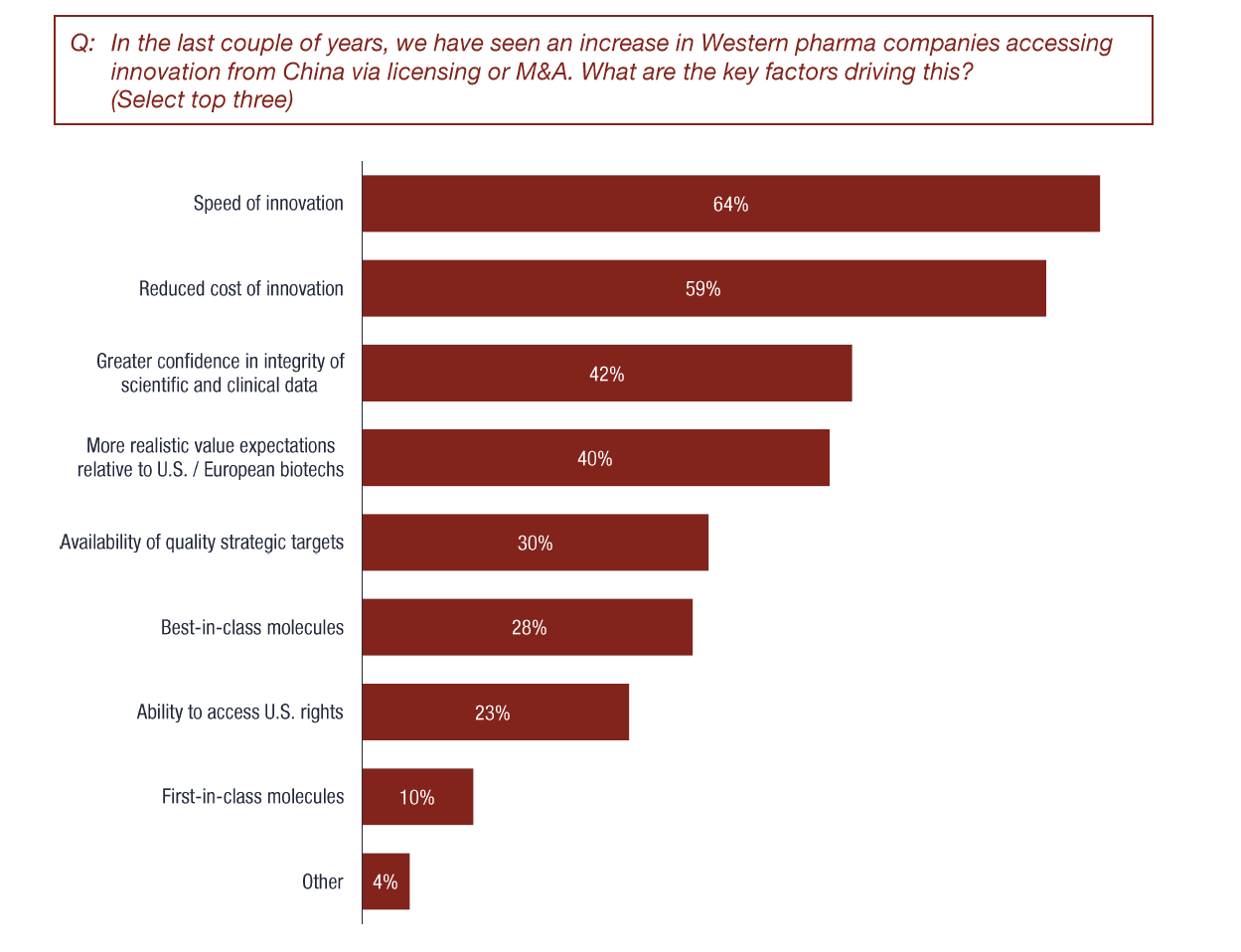

6. Significantly Greater Transaction Activity for Chinese Biopharmaceutical Assets Driven by Speed, Value, and Confidence in Data

Chinese assets remain a top priority for biopharmaceutical leaders who expect increased licensing and asset acquisition from China. Growing confidence in the integrity of Chinese clinical and scientific data, lower innovation costs, and greater speed of development have contributed to rising interest.